Five things that mattered in 2025

Market Insight

18/12/2025

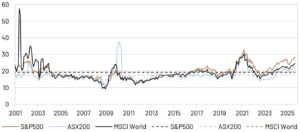

Table 1. Market returns as of 8 December 2025

1. The Fed cut rates in line with expectations

The Fed has cut rates broadly in line with expectations through 2025. At the beginning of the year, the Fed dot plots showed expectations for two rate cuts, before moving to three cuts priced in by June. Market pricing moved around but ranged between 2-4 rate cuts through 2025. The Fed cut rates for the third time in December, and the dot plots show Fed officials expect one cut in 2026. The rate cuts from the Fed have helped longer-dated Treasury yields to move lower over the course of the year, supporting decent returns in fixed income markets.

Chart 1: The US 10-year Treasury yield has been volatile but moved lower as the Fed cut rates.

Source: Bloomberg LP, Ascalon.

The Fed has shifted to focus on weaker jobs growth, despite inflationary pressures remaining solid. The uncertain outlook, delays in data due to the US government shutdown, and expectations for a more dovish Fed Chair next year, has complicated the policy outlook. Risks are now balanced around the Fed cutting rates less than the market anticipates in 2026, which could disappoint equity investors, and the Fed being forced to cut rates more as the labour market deteriorates, which would benefit fixed income but likely weigh on equity valuations.

2. Tariffs overwhelmed markets then underwhelmed economics

President Trump’s tariff policy caused a market meltdown on Liberation Day in April. But that feels like a distant memory with markets rallying around 35% from the trough in April. While tariff policy continued to play a big part in the first few months of his presidency, the extent of the tariffs was wound back by President Trump.

Despite tariffs spanning many regions and sectors, the economic fallout was short of investor concerns. Inflation did not spike dramatically, though US price growth has risen since April. Markets anticipated a sharp uptick in prices that never materialized, likely because tariffs were drip-fed as deals were struck and rescinded. Nonetheless, inflation has steadily re-accelerated, and margin expansion – that has driven equities higher – suggests that companies are passing on those costs to consumers.

The effective tariff rate remains at its highest level since the 1930s. And the process of tariff passthrough continues, leaving some upside to inflation. The legal challenges to the tariffs are unlikely to derail the tariff policy – we think they are here to stay.

But markets have now largely looked through tariffs as noise, notwithstanding some pockets of volatility. We suspect the full economic impact has not yet been realised, and stretched equity market valuations could still be challenged if growth slows further or prices increase more as tariffs continue to pass through to the economy.

Chart 2. Inflation had trended lower after the post-Covid spike, but has seen an uptick since April.

Source: Bloomberg LP, Ascalon.

3. Valuations stretched to record highs

Equity markets have traded well above long-run historic P/E ratios. By most measures, equities continue to be at valuations that look very stretched. That is true across small, mid and large caps, both inside and outside of the Magnificent 7. Despite some volatility through 2025, equity values have continued to surge higher. Earnings have been robust, but any misses in earnings or expectations were punished. Fundamentals do not necessarily support these stretched valuations, but market consensus has accepted that the equity market can keep expanding given a structural shift higher in medium-term earnings due to the rise of AI.

We continue to be sceptical that AI is a strong reason to accept structurally higher P/E ratios. Markets have been easily spooked when murmurs of an “AI bubble” reappear and the conversation shifts to whether AI can generate the productivity gains that it needs to justify current valuations. There is limited evidence currently that the adoption of AI will deliver sufficient profits to justify the scale of investments in its development. Equity markets have been whipsawed by these concerns, but then that is quickly forgotten, supported with a “buy-the-dip” mentality.

Chart 3. Equity price-earnings ratios remain well above long-term averages.

Source: Bloomberg LP, Ascalon.

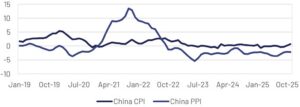

4. China remained in deflation

China’s economy has grappled with persistent deflationary pressures, reflected in a significant drop in producer prices and consumer inflation hovering around zero. In November, the consumer price index increased by 0.7% year-over-year, the highest it has been since February 2024. The producer price index continued its decline, falling by 2.2%, marking the 38th consecutive month of deflation in factory-gate prices.

The compounding effect of low growth in consumer prices against a backdrop of sustained producer price decreases signals major challenges for Chinese policymakers. They are faced with the task of stimulating demand in an economy burdened by industrial overcapacity and subdued consumer confidence. While some sectors, particularly retail, have seen slight recoveries, manufacturers are engaging in aggressive price-

cutting to manage excess supply, ultimately reflecting ongoing weak demand conditions. The government’s attempts to curb excessive price competition have been complicated by fears of job losses and further economic slowdown. The uneven recovery illustrates the challenge of stimulating economic activity while simultaneously containing persistent deflationary pressures.

Chart 4. Consumer price growth remains around zero while producer prices are deep in deflation.

Source: Bloomberg LP, Ascalon.

5. Australia’s inflation surprised to the upside.

Inflation in Australia trended lower through the first half of this year, after some stickiness put the Reserve Bank of Australia (RBA) on hold through 2024. Inflation has since seen a resurgence after falling to the RBA’s target in June. The earlier decline in inflation had provided some breathing room for the RBA to cut rates three times over 2025 in order to support the economy. Rate cuts did help stimulate demand, particularly in the housing market, but it now appears inflation was not fully under control.

The jump in inflation has raised important concerns for the RBA and Australia’s economy. Markets now expect no more rate cuts in the near-term, with pricing turning to potential rate hikes in 2026 to counter inflationary pressures. RBA Governor Bullock left the door open to rate hikes next year, and that could continue to weigh on bond and equity markets if inflation continues to accelerate.

Chart 5. Inflation in Australia has seen a dramatic uptick since bottoming in June.

Source: Bloomberg LP, Ascalon.