How your portfolio should be positioned entering the Fed’s first rate cut

Market Insight

02/10/2024

US inflation is under control. Fed Chair Powell has confirmed rate cuts will come in September. But the recent deterioration in the US labour market has opened the door to the risk of a 0.50% rate cut instead of a 0.25% rate cut. Against this backdrop, US equity market volatility has increased and US Treasury yields have moved lower. What can investors do to position for the beginning of the Fed’s rate cut cycle?

The Fed is going to cut – why is the magnitude important?

Markets are divided over whether we get a half or quarter percent cut when the Fed meets in September. Risk sentiment could rally as markets cheer the first rate cut, whatever the size. But if the Fed only cuts by 0.25%, it risks falling behind the curve if the economic slowdown deepens. On the other hand, there is a risk the Fed spooks the market if it cuts 0.50%. Investors may wonder what the Fed sees on the horizon that has forced it to implement “emergency” rate cuts this early in the rate cut cycle.

What should the Fed do?

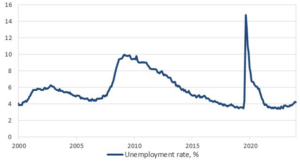

I have been worried about the economic slowdown for some months. Three key indicators have started to flash red or amber signals for recession. First, the change in the unemployment rate is consistent with rates that have historically signaled recession.

Chart 1: The unemployment rate is moving higher – historically a worrying indicator.

Source: Bloomberg LP, Oreana.

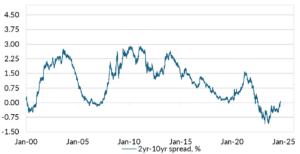

Second, the yield curve (the difference between the 10-year and 2-year Treasury yield) has normalized back to positive from more than two years of inversion. The normalization in the yield curve has historically been a recessionary signal.

Chart 2: The normalising yield curve is a worrying signal.

Source: Bloomberg LP, Oreana.

And third, the manufacturing PMI remains at levels that are consistent with sub-trend economic growth – albeit not quite signaling recession. It also suggests that S&P500 sales growth could be set for a further slowdown.

Chart 3: Manufacturing PMI is at below-trend levels, with risk to equity sales.

Source: Bloomberg LP, Oreana.

I think the Fed needs to get on with it. A 0.50% rate cut, followed by further rate cuts in the next few months, will likely be necessary to help prevent a harder landing. A 0.25% rate cut and steady as she goes approach will materially lower the likelihood we get a soft-landing.

What are the key risks?

First, let’s identify the key risks. It is not whether we get a 0.25% or 0.50% rate cut. And it is not even whether we have a recession or not.

I think the key risk is, is the equity market adequately reflecting the slowing economic growth. And if not, can the Fed cut aggressively enough to push growth higher in the near-term.

Let’s take the key risk first. US equity markets continue to trade at extended valuations relative to history. Earnings growth is projected to be in the double-digit range. But economic growth is slowing rapidly. And that means margins will probably need to expand. How could that happen? Perhaps by a reduction in labour costs, which could further drive up unemployment and drag revenue growth! I worry that equity markets are pricing a reacceleration in growth which is going to be difficult to achieve, even with rate cuts.

So, can the Fed cut quickly enough to combat growth? Perhaps. This time could be different. But monetary policy historically has worked with long and variable lags. That is both when rates are on the way up, and when they are on the way down. In other words, even 1.00% of rate cuts before end-2024 could still leave the unemployment rate climbing towards 5.00% by early-2025.

So given these risks, why is the size of the cut important? A bigger cut will trigger market concerns around the key equity market risk. And I expect it will shine a light on the second risk, that is, that the Fed is behind the curve.

How can portfolios be positioned for the risks?

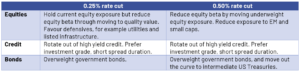

In table 1, I suggest positions that I expect will benefit most from the signal delivered by a 0.25% versus a 0.50% rate cut. In summary, being underweight credit and overweight government bonds, and defensively positioned in equities, is my preferred stance. But there are nuances. A smaller initial rate cut could prevent panic in the equity and credit markets, and deliver less of a boost to government bonds.

Table 1: Preferred positions ahead of the Fed rate cut.

Don’t panic!

Equity markets could move in either direction following the first rate cut. I would not chase any rally – it will simply stretch market valuations further. If equity markets fall, then there may be opportunities to add exposure at more attractive valuations. For those investors inclined to make changes ahead of the Fed, I think adding some government bonds makes the most sense, as we expect rates could fall further than is currently priced, driving government bond yields lower over the coming 12 months. But whichever way the Fed moves, it is important to remember not to panic.