Persistent Inflation and Uneven Growth

Market Insight

16/06/2026

The global economy is dealing with an inflation shock that may not have peaked yet. The impact has not been uniformly felt by different global economies. Parts of Asia and Australia have been more materially impacted. But the US has shrugged off the impact and growth has accelerated in Q2. This may mean that potentially divergent monetary policy could drive further volatility through markets over H2 2026. We continue to recommend diversification and portfolio resilience as key levers to improve outcomes over the horizon.

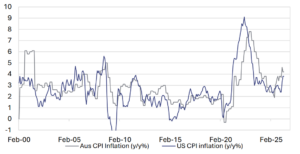

Higher oil prices have pushed up global inflation.

The global economy is currently facing what appears to be a relatively uniform inflation shock. Higher oil prices have flowed through relatively quickly to headline inflation. The extent that flows to underlying inflation is still uncertain. But most central banks will be reluctant to write this shock off as transitory after the experiences in the early-2020s.

Chart 1: Headline inflation is starting to move materially above central bank targets.

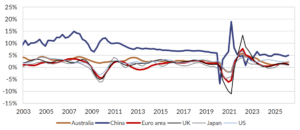

Economic growth has slowed, but not uniformly.

Higher oil prices and higher inflation represent a potential shock to global growth. Already, the EU, UK and Japan are experiencing slower economic growth. The US and Australia, on the other hand, have had their most recent economic growth numbers flattered by capex spending on data centres. The US has been particularly resilient, with jobs growth improving and households remaining resilient as a result. China’s economic growth has also helped support global growth.

Chart 2: Global economic growth has so far proven resilient to higher inflation and oil prices.

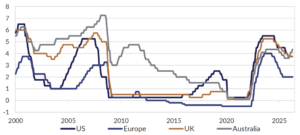

The monetary policy outlook has diverged.

The uneven economic impact is starting to show up in divergent monetary policy. Policy expectations have changed rapidly through 2026, and are quite different across different geographies. In Australia, the RBA has moved from an easing bias to a series of rate hikes. Further rate hikes are possible. However, we suspect the RBA will be very cautious in adding more hikes after the unemployment rate unexpectedly jumped to 4.5% from 4.3%. Europe is set to hike rates to control inflationary pressures. Meanwhile in the US, the market has moved rapidly to reprice the risk of policy rate cuts to expecting one full 0.25% rate hike this year, with another expected in 2027. We think a rate hike is less likely than the market is pricing, although that is predicated on weakness starting to show through consumer spending and in the jobs market.

Chart 3: Central bank policy rates look likely to start diverging through 2026.

Manage risks and volatility through deliberate diversification and portfolio resilience.

Diverging monetary policy expectations can flow through markets in multiple ways.

1) Government bond yield curves move to reflect policy. We think this has largely been priced in the Australian government bond market. Higher yields leave these assets looking relatively attractive. US Treasury yields may still have room to reprice higher, introducing some more risk in these assets.

2) Higher interest rates can increase the discount rate for equities. A higher discount rate reduces the present value of future cash flows, particularly for companies that are currently unprofitable or are unlikely to pay dividends until a long way in the future. Given current valuations, higher interest rates may cause more volatility in equity markets.

3) Currencies can act as a pressure release valve for policy differences. The Australian dollar had increased around 11% versus the US dollar over the past year as markets looked favourably on higher Australian rates. But US rates have increased rapidly recently, reducing the attractiveness of the AUD. While the AUD looks reasonably fairly valued at current levels, we suspect there is more two-sided risk than the market appreciates. We expect volatility to remain a feature of this market in the near-term. We have been working carefully with investors to introduce appropriate diversification in portfolios to reduce exposure to one or two major macro consensus views that are dominating portfolio returns. That includes building resilience to more adverse outcomes than are currently priced across asset markets. We continue to think that focusing on diversification and building quality exposures across different asset classes will benefit investors through what could be a volatile period for markets.

Disclaimer: This presentation has been prepared by Oreana Private Wealth, a division of Oreana Financial Services(Oreana) for general information purposes only, without taking into account any potential investors’ personal objectives, financial situation or needs. This information consists of forward-looking statements which are subject to known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements to be materially different from those expressed or implied. Past performance is not a reliable indicator of future performance. Neither this document nor any of its contents may be used for any purpose without the prior consent of Oreana. Anyone reading this report must obtain and rely upon their own independent advice and inquiries.

Limitation of liability: Whilst all care has been taken in preparation of this report, to the maximum extent permitted by law, Oreana will not be liable in any way for any loss or damage suffered by you through use or reliance on this information. Oreana’s liability for negligence, breach of contract or contravention of any law, which cannot be lawfully excluded, is limited, at Oreana’s option and to the maximum extent permitted by law, to resupplying this information or any part of it to you, or to paying for the resupply of this information or any part of it to you.