What to do if the Everything Rally is over

Market Insight

25/02/2026

The post-Liberation Day rally from mid-April dragged most asset classes higher. US equity valuations stretched to historic highs. Credit spreads narrowed to multi-decade tights. Bitcoin surged, gold and silver prices increased parabolically, and even government bonds, which sold off into the year-end, largely added value to investor portfolios.

Markets are now experiencing a bout of cross-asset volatility in early 2026 that feels uncomfortable given the strong gains in 2025. This month we look at whether the everything rally is done, and what investors can do to manage two-sided market risk.

Is the everything rally over?

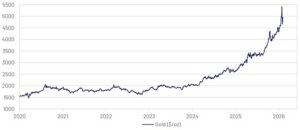

Gold experienced a greater than 20% peak to trough drawdown. Silver fell more than 40% at one point. From its peak above USD100,000, bitcoin has now declined more than 40%. And the S&P500 tech sector, the driver of most returns for the past couple of years, is more than 10% from its peak as elevated valuations have been met with questions around the future of software as a service (SAAS) and the demand for AI.

Chart 1: Gold has slumped after reaching record high prices in early 2026

Source: Bloomberg LP, Ascalon.

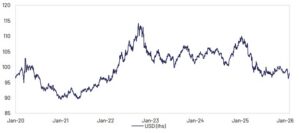

At the same time, the US dollar has attracted inflows helping to lift the currency from its recent troughs. The USD had traded sideways for most of 2025, before reaching a new multiyear low in late-January. The low coincided with a consensus narrative on the so-called “debasement trade”. This view suggested that investors would buy gold and equities, and sell the USD and US Treasury bonds, as they worried about US deficits, the US dollar’s global reserve status, and geopolitical risk. The recent inflows suggest this trade may be under question from investors, capping the everything rally.

From an economic perspective, the everything rally has also come under challenge from the risk of a less dovish than anticipated US Federal Reserve. The newly nominated Fed Chair, Kevin Warsh, has historically been an inflation hawk, and markets worried that fewer rate cuts could be delivered this year. Relatively higher interest rates pressures equity valuations, credit spreads and gold prices. If the Fed does deliver fewer cuts than anticipated, then market volatility is at risk of remaining elevated.

Chart 2: The USD has rallied amid risk-off sentiment

Source: Bloomberg LP, Ascalon.

Or could the rally keep running?

The market movements have nonetheless not moved sufficiently violently to erase the gains from the past 12 months. And while valuations look stretched, historically this has not been a catalyst for a correction.

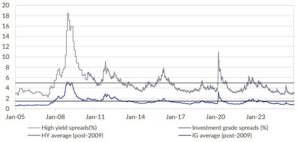

Outside of the large moves in gold, silver and bitcoin, market prices have not broken to levels that would be consistent with the bull market ending. Credit spreads, particularly sub-investment grade, have not widened aggressively. Government bond yields have not moved dramatically lower in signs of severe risk-off sentiment. This suggests markets may not be at a tipping point yet.

Economic data have so far proven resilient. While the labour market is clearly cooling, and consumer confidence is historically weak, household spending and business investment remains resilient. Corporate margins have expanded, offsetting some weakness in sales. Earnings growth has been near double digit rates for several quarters. That provides some support to the notion that stretched valuations could normalise via a combination of steady price gains and reasonable earnings growth, rather than a calamitous decline in the price level. However, we remain cautious given elevated valuations and the strength of recent returns. Price gains may continue, but we suspect equity returns on offer will be closer to historic outcomes than the recent double-digit gains in equities.

Chart 3: Credit spreads remain tight despite volatility in other markets.

Source: Bloomberg LP, Ascalon.

What can investors do to manage risk?

Use scenarios to manage risk: Scenario analysis and stress tests help quantify potential risks when the outlook is exceptionally uncertain. This month, we release our Medium Term Outlook which includes a discussion of two scenarios and their implications for portfolios.

Review diversification and rebalance consistently: The range of potential outcomes is wide. A key action for investors is to take advantage of deliberate diversification and rebalance portfolios to target weights on a consistent basis.

In a low conviction environment, take low conviction positions: Elevated volatility and uncertainty may not adequately reward heroic tilts away from strategic asset allocation. We suggest sticking close to neutral.

Understand the extent of risk in your portfolio: The strong returns enjoyed over the past three years may have resulted in unintended risks within portfolios. This could include concentrations in one or more sectors or markets, higher risk exposures to certain types of credit, or sensitivity to certain macro drivers. We suggest examining portfolios through multiple lenses to help manage risk.

Remain invested: Even though uncertainty is elevated, resist the temptation to move to cash and sit out the volatility. Trying to time the market is unlikely to deliver outcomes that achieve most investment objectives. Instead, remain invested and consider the actions above to manage risk in this uncertain environment.